Inside the $1.3B Trading Scandal No One Saw Coming: Case Study

What Happened

In one of the largest market manipulation scandals in modern finance, Man Group’s brokerage arm, which was eventually folded into MF Global, was linked to the infamous Forex Fixing Cartel. A network of traders at major banks, including Man Group’s affiliates, coordinated trades to manipulate benchmark currency rates for profit. The main focus was the 4 PM London Fix, a critical pricing moment used by investors and asset managers worldwide.

This collusion not only distorted currency prices but also damaged institutional trust and triggered global regulatory scrutiny. Over time, the total financial exposure and penalties related to poor oversight and compliance weaknesses at affected institutions, including those tied to Man Group, topped $1.312 billion.

How It Happened

The scandal wasn’t a fast-moving fraud, it was a systemic failure that built up over years. Here’s how it occurred:

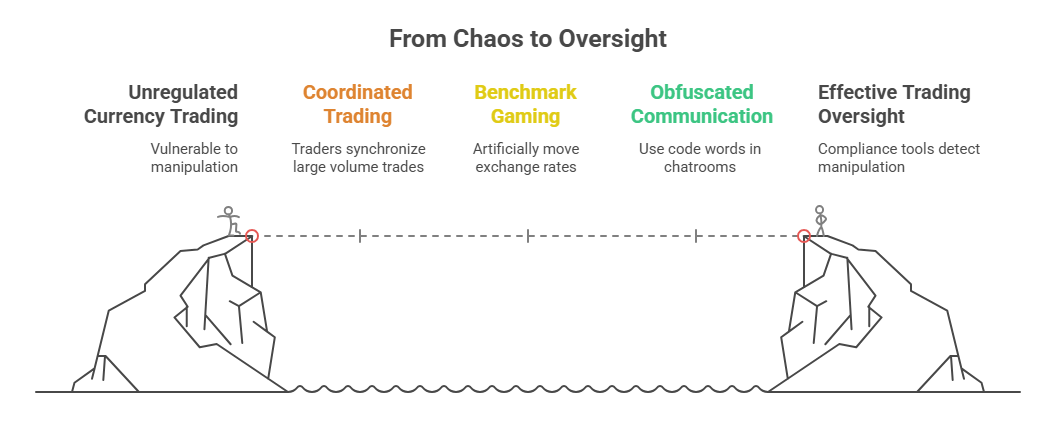

Coordinated Trading Behavior: Traders from different banks used private chat rooms (e.g., “The Cartel,” “The Bandits’ Club”) to synchronize large volume currency trades at benchmark times.

Benchmark Gaming: By concentrating their trades around the fix window (especially the 4 PM London Fix), they artificially moved exchange rates to benefit their positions.

Ineffective Internal Oversight: Despite massive trading volumes and unusual patterns, internal compliance tools either failed to detect the manipulation or lacked authority to act.

Obfuscated Communication: Traders used code words and insider slang in chatrooms, making it difficult for traditional compliance teams to catch the manipulation.

The failure wasn’t just technical, it was cultural and procedural, driven by misaligned incentives and absent real-time controls.

How It Could Have Been Prevented

Several practical measures could have prevented the scandal or at least caught it much earlier:

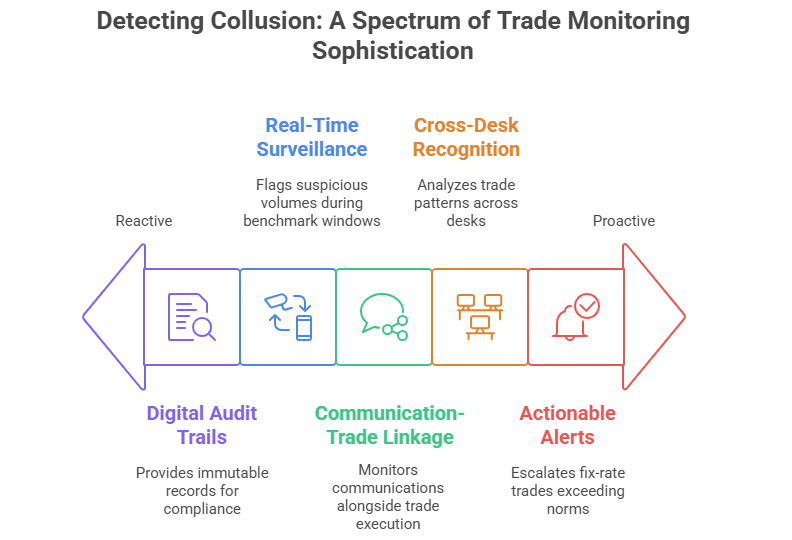

Real-Time Trade Surveillance: A system capable of flagging suspicious volumes during benchmark windows would have exposed the coordination.

Communication-Trade Linkage: Monitoring communications alongside trade execution could’ve revealed patterns in chat behavior aligning with rate manipulation.

Cross-Desk Pattern Recognition: Tools analyzing trade patterns across traders, desks, and geographies would have picked up on the collusion’s structure.

Actionable Compliance Alerts: Automated escalation to compliance officers when fix-rate trades exceeded statistical norms could have served as an early warning system.

Digital Audit Trails: Immutable records of trade activity would have empowered compliance teams with evidence to take action.

The tools to prevent such manipulation existed, but they were either not in place or not integrated across the trading lifecycle.

How Sequenxa Can Solve the Problem

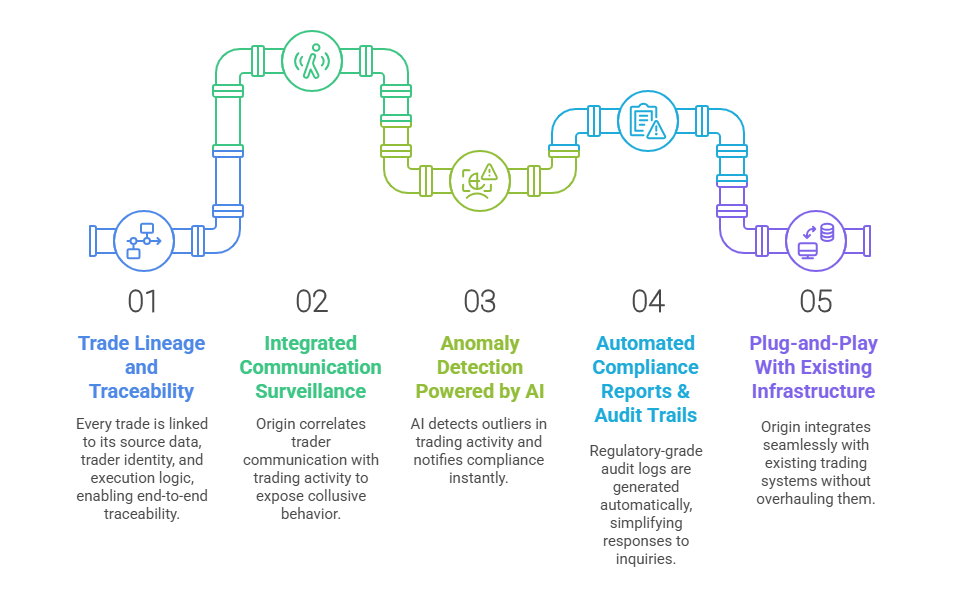

Sequenxa’s Origin platform offers the precise controls and visibility that legacy systems lacked, and regulators now demand:

Every trade is linked to its source data, trader identity, and execution logic, enabling end-to-end traceability. This visibility reveals who did what, when, and why, crucial in detecting manipulated trades.

Origin correlates trader communication (chat, email, voice) with trading activity. This linkage can expose collusive behavior and flag suspicious language patterns in real-time.

Using predictive analytics, Origin detects outliers, such as unusual volume surges or timing anomalies around fix windows, and notifies compliance instantly.

Regulatory-grade audit logs are generated automatically, simplifying responses to inquiries and enabling fast, confident internal investigations.

Whether you're using Bloomberg, Refinitiv, or a custom OMS/EMS, Origin integrates seamlessly without overhauling your existing trading stack.

By deploying Sequenxa Origin, financial institutions can monitor, prevent, and respond to trading misconduct before it escalates into billion-dollar scandals.

Key Lesson

The MAN Group case proves that weak oversight and fragmented data create space for manipulation. Real-time monitoring, connected communication and trade data, and proactive compliance are no longer optional, they’re essential.

With platforms like Sequenxa Origin, firms can prevent misconduct before it happens, protect their reputation, and avoid billion-dollar penalties.